Prajna Capital |

| Bajaj Allianz General Insurance Posted: 09 Oct 2015 04:37 AM PDT Bajaj Allianz General Insurance Co. Ltd.Bajaj Allianz General Insurance Company Limited is a joint-venture between Allianz SE, one of the world's largest life insurance companies and Bajaj Finserv Limited (recently de-merged from Bajaj Auto Limited).Allianz SE is a leading insurance conglomerate globally with 115 years experience in over 70 countries. It is one of the largest asset managers in the world, managing assets worth over a trillion euros. Bajaj Allianz General Insurance offers the traditional general insurance covers in motor insurance, asset insurance, health insurance, travel insurance, and corporate insurance. Apart from these traditional insurance products, Bajaj Allianz also has some unique insurance products such as personal accident cover for Amarnath yatris, film insurance, event management cover, and sports & entertainment insurance. Best Tax Saver Mutual Funds or ELSS Mutual Funds for 2015

1. BNP Paribas Long Term Equity Fund 2. Axis Tax Saver Fund 3. IDFC Tax Advantage (ELSS) Fund 4. ICICI Prudential Long Term Equity Fund 5. Religare Tax Plan 6. Franklin India TaxShield 7. DSP BlackRock Tax Saver Fund 8. Birla Sun Life Tax Relief 96 9. Reliance Tax Saver (ELSS) Fund 10. HDFC TaxSaver

Invest Rs 1,50,000 and Save Tax under Section 80C. Get Good Returns by Investing in ELSS Mutual Funds Online

Invest in Tax Saver Mutual Funds Online For further information contact Prajna Capital on 94 8300 8300 by leaving a missed call --------------------------------------------- Leave your comment with mail ID and we will answer them OR You can write to us at PrajnaCapital [at] Gmail [dot] Com OR Leave a missed Call on 94 8300 8300 |

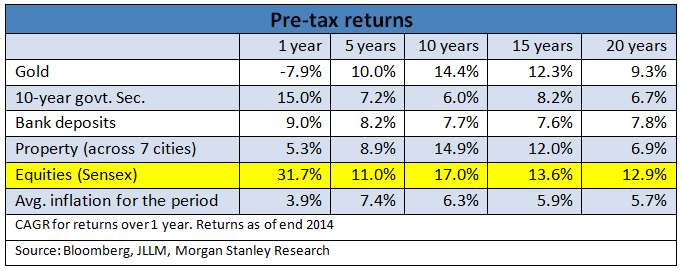

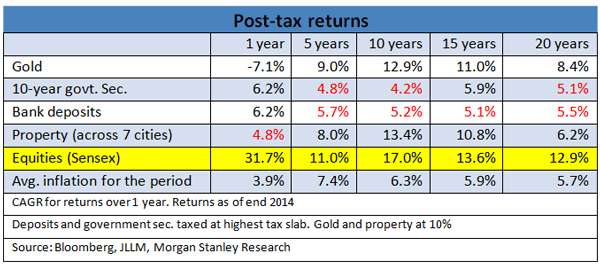

| Posted: 09 Oct 2015 02:31 AM PDT Mutual Funds vs Other Investments  |

| Posted: 09 Oct 2015 12:41 AM PDT Invest Mutual Fund Online

You have a lump sum in hand and you wish to invest in equity funds. However, you have heard a lot of talk about investing in equity funds through Systematic Investment Plans (SIPs) because they help average costs, ensure you do not ill-time the market, and help you invest in small sums, besides giving you many other advantages. So, should you invest the money you have in hand in one go, or let it remain in your bank account and then do an SIP? There is no harm in investing a lump sum amount. For all you know, compounding, over the long term, could work better with lump sum. However, make sure you fulfill all of these three criteria if you want to invest in one go. Else, SIP is the way to go. #1: You invest for the long term According to past data, ideally, if you have a time frame of 12 years or more, you can consider lump sum investing (provided you satisfy the other two conditions that follow). So, what is the sanctity behind 12 years? Is it because only 12 years can be called long term? Yes, partly that, but more because that is the time frame over which the markets did not have any negative return periods. In other words, the chances of your earning negative returns would be nil over any 12-year buckets from 1980 till date, irrespective of which date you had invested a lump sum. This 12-year period we are talking about is, of course, subject to change. It could be 10 years or 15 years. It varies based on the time period we consider. Hence, again, different market phases (bull or bear) play a role in window dressing this, or in removing the veil.

#2: You really know the lump sum you need No, there is no debate here on what amount can be termed lump sum – Rs. 50,000 or Rs. 5 lakh. What I mean here is whether the lump sum is sufficient to meet the goal. When you invest a lump sum, there is more reason why you should have a goal/target for it. The tendency to have a goal is better when you do an SIP, where you say – "I will invest Rs. 10,000 a month over the next 10 years towards my daughter's education," or any other such goal. When you do that, you have a fair idea of what to expect – not just when it comes to returns, but also when it comes to your own savings too. For instance, you know, even without any compounding of returns, that you will save (your investment cost) Rs. 12 lakh (Rs. 10,000 a month for 10 years) over this period. However, with lump sum investing, you do not tend to think about what the investment will grow to, and hence, there are chances that you would never top it up to ensure that you have a comfortable kitty. For instance, let's say you invested Rs. 5 lakh for 10 years, and it earned 12 per cent a year and grew to Rs. 15.5 lakh. By the 8th year, it suddenly struck you that you can use this money for your kid's college education which is, say, two years away. You do a rough calculation and realise you need Rs. 25 lakh. How much would the Rs. 5 lakh of investment fetch you? Just Rs. 15 lakh! This means you fall short by Rs. 10 lakh. In two years, you have to make this good by investing a lump sum of Rs. 8 lakh (at the same rate of return assumed), or by investing Rs. 38,000 a month for the next two years through an SIP – both of which may seem challenging, especially if you do not have the habit of regularly saving. Even if you manage this, a 2-year equity route could kill your ambitions. This is where, in reality, not having an idea of how much lump sum is good enough for you can hurt you. In this case, had you known you would need Rs. 25 lakh, your lump sum invested 10 years ago should have been Rs. 8.5 lakh, provided you had that kind of surplus. SIPs give you the chance to gradually increase your savings, without hurting your cash in hand too much, and without hurting you in the market. But if you know your goal, you have the sum to spare, and of course, to satisfy our other criteria, lump sums can be good. #3: You can stay calm Yes, in rallying markets, it is likely that you can enjoy super high returns from your lump sum investments. But if you can stay calm in market crashes such as the one in 2008, when you see your investment fall by over 50 per cent, then lump sum investing is for you. But remember, a single massive fall such as 2008, takes a lot of time for your fund to recover when you invest through a lump sum, as opposed to the SIP way of investing. Just to give you an example, had you invested in Reliance Equity Opportunities on January 1, 2008 (just before the market slide that year), you would now be sitting on a healthy annual rate of return of 14 per cent. But had you started your SIP on the same day in 2008 and continued till date, your returns would have been 23.5 per cent annually (IRR). That means there is still an opportunity loss in not averaging in a bad market like 2008. If you will not do that comparison and stay happy with the returns you see, good for you. Transfer systematically So, what do you do if you have a large sum in hand, but cannot invest lump sum if you do not fit into any of these criteria? Invest in a liquid fund and do a Systematic Transfer Plan (STP). Your lump sum in a short-term debt fund (liquid or ultra short term) will earn higher returns than your savings bank interest, and you will get to average by entering markets systematically. The one choice you have here is to take a shorter period of averaging (6-12 months) if the amount is not too large, provided you have a 7-year plus time frame. Else, average over at least 36 months. Best Tax Saver Mutual Funds or ELSS Mutual Funds for 2015

1.ICICI Prudential Tax Plan 2.Reliance Tax Saver (ELSS) Fund 3.HDFC TaxSaver 4.DSP BlackRock Tax Saver Fund 5.Religare Tax Plan 6.Franklin India TaxShield 7.Canara Robeco Equity Tax Saver 8.IDFC Tax Advantage (ELSS) Fund 9.Axis Tax Saver Fund 10.BNP Paribas Long Term Equity Fund

You can invest Rs 1,50,000 and Save Tax under Section 80C by investing in Mutual Funds

Invest in Tax Saver Mutual Funds Online - For further information contact Prajna Capital on 94 8300 8300 by leaving a missed call --------------------------------------------- Leave your comment with mail ID and we will answer them OR You can write to us at PrajnaCapital [at] Gmail [dot] Com OR Leave a missed Call on 94 8300 8300 --------------------------------------------- Invest Mutual Funds Online Download Mutual Fund Application Forms from all AMCs |

| You are subscribed to email updates from Prajna Capital - An Investment Guide. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment