Prajna Capital |

| LIC Nomura MF Tax Plan dividend Posted: 04 Dec 2015 03:53 AM PST LIC Nomura Mutual Fund has announced dividend under the following schemes:

LIC Nomura MF Tax Plan-D | 0.5 | LIC Nomura MF Tax Plan Direct-D | 0.5 | The record date has been fixed as December 08, 2015.Best Tax Saver Mutual Funds or ELSS Mutual Funds for 2015

1. BNP Paribas Long Term Equity Fund 2. Axis Tax Saver Fund 3. IDFC Tax Advantage (ELSS) Fund 4. ICICI Prudential Long Term Equity Fund 5. Religare Tax Plan 6. Franklin India TaxShield 7. DSP BlackRock Tax Saver Fund 8. Birla Sun Life Tax Relief 96 9. Reliance Tax Saver (ELSS) Fund 10. HDFC TaxSaver

Invest Rs 1,50,000 and Save Tax under Section 80C. Get Good Returns by Investing in ELSS Mutual Funds Online

Invest in Tax Saver Mutual Funds Online For further information contact Prajna Capital on 94 8300 8300 by leaving a missed call --------------------------------------------- Leave your comment with mail ID and we will answer them OR You can write to us at PrajnaCapital [at] Gmail [dot] Com OR Leave a missed Call on 94 8300 8300 | ||

| Posted: 04 Dec 2015 03:34 AM PST Funds that withstand downturns better tend to yield higher returns The current slump in the stock market, after a sustained upward march for close to two years, has caught several equity funds on the wrong foot. The current situation proves a fund should not be judged merely by its performance when the broader market is on a roll. What makes a fund a solid bet is its performance when the chips are down. Funds that withstand downturns better tend to yield higher returns over the long term. Very few funds boast the ability to deliver returns higher than the market during a bull phase, while limiting losses during a downturn. These funds emerge as the outperformers over time. To test this argument, we considered the up and down capture ratios of different categories of equity funds from September 1, 2010 to August 31, 2015, a period when funds had to handle varied market climates. The ratio shows how much of the market's move was captured by the fund. The upside capture ratio indicates the percentage of the market's gain that was captured by the fund while the downside capture ratio reveals the percentage of the market's fall that was captured by the fund. So, while an upside capture of over 100% indicates that a fund outperfor med the benchmark or category average during periods of positive retur ns, a downside capture below 100% indicates that a fund lost less than its benchmark or category average during periods that the market was in the red. For instance, if during a period, the market moved up by 20%, but the fund moved up by 25%, it means that the fund captured 125% (25% of 2 0 % ) o f t h e m a rke t 's m ove.Similarly, if the market went down by 10% and your fund value drops by 8%, the fund would have a downside capture of 80%. Each fund's performance has been compared with its respective benchmark index. The data provided by Morningstar India shows that over the past five years, the funds with a lower downside capture ratio have emerged among the top performers. Across categories, funds that have limited the downside well have fared better than their category average. These funds have stood out over this 5-year period because it was a time when the markets went through significant ups and downs. For instance, in the large-cap space, funds with a downside capture of less than 100% yielded annualised return of 10.23% on average in the 5 year period, compared to the category average of 9.61%. On the other hand, funds that captured more than 100% of the market downside during this period averaged retur n of 6.67% only.Many of the funds with a high downside capture boast of more than 100% upside capture. They generated higher return than the market during periods of price rise--yet lost out ultimately owing to the bigger hit taken during downturns. Similarly, in the mid-and-small cap category , funds with a downside capture of more than 100% averaged annualised return of 7.37% over the 5 years against the category return of 16.32%. In contrast, funds that kept the downside in check delivered 17.13% annualised return. SBI Small & Midcap Fund, for instance, only captured 91% of the market upside during these 5 years, but its extremely low downside capture helped it be a table-topper. Funds which suffered from high downside capture were among the best in terms of upside capture, but lagged behind other funds over the entire time period. The same trend is visible in the flexi-cap space. It is clear from this analysis that investors would do well to side with funds that are adept at providing a buffer against market declines and not those which give the highest returns when the going is good. While managing downside well is critical, the fund should have a decent upside capture as well, even if not among the highest. Long term performance boils down to how the fund manages the downside. Even if the fund boasts of the ability to capture 140% of the market upside, but sees similar value erosion during downturns, it will not come out healthy over time. However, this doesn't mean that the fund's ability to ride a market rally should be overlooked. Best Tax Saver Mutual Funds or ELSS Mutual Funds for 2015

1.ICICI Prudential Tax Plan 2.Reliance Tax Saver (ELSS) Fund 3.HDFC TaxSaver 4.DSP BlackRock Tax Saver Fund 5.Religare Tax Plan 6.Franklin India TaxShield 7.Canara Robeco Equity Tax Saver 8.IDFC Tax Advantage (ELSS) Fund 9.Axis Tax Saver Fund 10.BNP Paribas Long Term Equity Fund

You can invest Rs 1,50,000 and Save Tax under Section 80C by investing in Mutual Funds

Invest in Tax Saver Mutual Funds Online - For further information contact Prajna Capital on 94 8300 8300 by leaving a missed call --------------------------------------------- Leave your comment with mail ID and we will answer them OR You can write to us at PrajnaCapital [at] Gmail [dot] Com OR Leave a missed Call on 94 8300 8300 --------------------------------------------- Invest Mutual Funds Online Download Mutual Fund Application Forms from all AMCs | ||||||

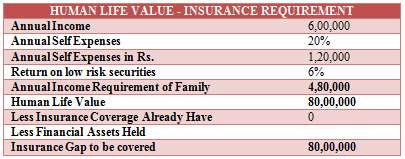

| Posted: 04 Dec 2015 02:04 AM PST Securing your family's well-being is one of the most important goals in life. One way to ensure this is by planning for their protection against uncertain events through insurance. An untimely death can cause a major setback to your family – both emotionally as well as financially, especially if you are their sole breadwinner. What is Human Life Value? Human Life Value (HLV) is a way of deciding how much life insurance you actually need. Your income, expenses, and number of employable years, along with the inflation adjusted cost of your future expenses will be taken into consideration here. There are two ways to calculate HLV:

Income Replacement Method Let's say your income is Rs. 6,00,000 per annum. Let's keep aside 20% of this for personal expenses like petrol, or other essential recreational expenses. Your family needs Rs. 4,80,000 for their regular expenses. You don't have any financial assets under your name. In this case, we need to have a corpus of Rs. 80,00,000 as fixed deposit which provides an interest of 6% per annum. In this case, your HLV is Rs. 80,00,000 presuming you don't have any existing insurance and you haven't made any investments earlier. The same would be less if you have already taken any insurance, or have any financial investments in your name.

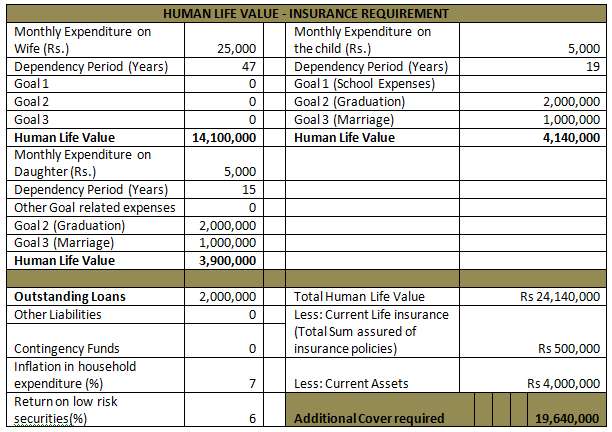

Need Analysis Method In this method, you have to first identify your liabilities like home loans, car loans or personal loans. There could also be other liabilities like the expenses of your wife and kids, goals like your children's higher education, their marriage in the future, etc. Based on this, you can find out the insurance gap in your life. If all your liabilities are covered by all your accumulated assets, then you don't need insurance. Remember: For example, if your HLV is Rs. 1,00,00,000 and your investments in various asset classes (properties and other financial assets) is Rs.1,00,00,000, then your accumulated assets are backing your HLV and you don't require insurance.

In the illustration given above, the monthly expenses of a man and his family are Rs. 25,000. His wife is 38 years old and her life expectancy is 85 years. Thus, the family's needs are to be met till the life expectancy of the spouse is met. He has two children and he wishes to save money for their higher education and marriage, which will cost him Rs. 20,00,000 and Rs. 10,00,000 respectively for each child. The children's ongoing expenses are Rs. 5,000 per month for each child. He also has a home loan liability of Rs. 20,00,000. In the above case, the HLV works out to be close to Rs. 2.5 crore. He already has taken insurance coverage to the tune of Rs. 5,00,000 and he has accumulated assets worth Rs. 40,00,000. The insurance gap identified in the above illustration is Rs. 1.9 crore.

Best Tax Saver Mutual Funds or ELSS Mutual Funds for 2015

1.ICICI Prudential Tax Plan 2.Reliance Tax Saver (ELSS) Fund 3.HDFC TaxSaver 4.DSP BlackRock Tax Saver Fund 5.Religare Tax Plan 6.Franklin India TaxShield 7.Canara Robeco Equity Tax Saver 8.IDFC Tax Advantage (ELSS) Fund 9.Axis Tax Saver Fund 10.BNP Paribas Long Term Equity Fund

You can invest Rs 1,50,000 and Save Tax under Section 80C by investing in Mutual Funds

Invest in Tax Saver Mutual Funds Online - For further information contact Prajna Capital on 94 8300 8300 by leaving a missed call --------------------------------------------- Leave your comment with mail ID and we will answer them OR You can write to us at PrajnaCapital [at] Gmail [dot] Com OR Leave a missed Call on 94 8300 8300 --------------------------------------------- Invest Mutual Funds Online Download Mutual Fund Application Forms from all AMCs |

| You are subscribed to email updates from Prajna Capital - An Investment Guide. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment