Prajna Capital |

- Tax Benefits of Life Insurance and Health Insurance Policies in India

- Improve your Bad CIBIL Score

- Mutual Fund SIP Return Tips

| Tax Benefits of Life Insurance and Health Insurance Policies in India Posted: 10 Nov 2015 04:03 AM PST Insurance Policies Tax BenefitsInsurance Policies completely live up to the Phrase "Icing on the Cake!!!". Insurance policies do not only safeguard your life and health but also gives you tax benefits for the premium paid and maturity amount received. The very first step of a successful tax or financial planning start with getting yourself adequately Insured.

Let's see how you can save tax through Insurance Policy in India. Life Insurance Tax BenefitLife Insurance Policy is a traditional plan which includes term plans, ULIPS (unit linked insurance plans), money back and whole life cover plan. All the plans except term plan are mix of investment as well as insurance, term plan gives your pure insurance. But for the purpose of taxation all these plans are treated same and the tax treatments of all plans are same. Tax benefit on Life Insurance Policy in IndiaPremium Paid

2. On Maturity: Insurance Sum received on maturity is completely tax-free u/s 10 of the I-T Act. 3. On the Death of the Policy Holder: Insurance Sum received on the death of the assesse by his family or legal heirs is completely tax-free u/s 10 of the I-T Act. But a death certificate of the policy holder is required to be given to the insurer along with the other documents to claim the insurance amount. Health Insurance Tax Benefit or Mediclaim PolicyThe earning members of most of the Indian households are one or two while they have dependent children and dependent parents to look after. Due to increasing cost of medical treatment Health Insurance Policy or mediclaim policy has become must for every household. Along with covering the cost of the medical expenses it also gives you tax benefits. Tax benefit on Health aka Medical Insurance IndiaPremium Paid:Under Section 80D of the I-T Act assesse can claim the deduction for premium paid for Health Insurance or Mediclaim Policy for up t0 Rs.25,000 p.a. for himself, his spouse and his children. In case he also buys Health Insurance or Mediclaim Policy for his dependent parents than a separate deduction of Rs.25,000 will also be allowed for deduction and if his parents are senior citizen (60 years or above) than deduction will be of Rs.30,000. This means an assesse can get maximum benefit of Rs.55,000 u/s 80D. But to claim the deduction, few conditions have to be met:

Insurance Sum Received:Any sum received from the insurer against the health insurance policy or mediclaim policy does not constitute your income and thus would be exempt. The sum received from insurer is mere a reimbursement of expenses you have incurred. Thus it would completely be tax-free. Suppose you have received Rs.1 lakh against the mediclaim policy than this amount would not be taxable as your income, since this is just a settlement of the medical expenses you have already incurred and there is no element of the income in your claim. Many of the Insurance Companies have started Cashless Health Insurance Schemes, under which you don't need to pay any amount to the medical institutes. The medical bills are directly paid to the medical institute by TPA/Insurance Company. Tax Benefits of Pension PlansPension Plans or Annuity Plans have a very different tax treatment from life insurance or health insurance plans. Tax benefit on Pension Plans in IndiaPremium Paid:

Sum Received1. On Surrendering the Policy before Maturity: In case the policy is surrendered before the maturity there will be two effects:

2. On Maturity: On maturity the 1/3 of the sum received will be tax-free and remaining 2/3 of the amount shall be used to purchase annuity plans as specified by IRDA. The monthly income from this annuity plan will be added to your income and taxed accordingly. 3. On the Death of the Policy Holder: The sum received by the family or legal heirs upon death of the policy holder is completely tax-free under section 10(10D) of the I-T Act. Due to the tax benefits Insurance Policies have become one of the most favoured investments of Indians but one has to read the terms carefully before going for any policy. Insurance Sum Received:1. On Surrendering Policy before maturity: In case the policy is surrendered before the maturity than the whole sum received from the Insurer will be taxable, if 5 premiums have not been paid. If you have surrendered the policy after paying 5 premiums than the amount received from the insurer would be tax-free. Best Tax Saver Mutual Funds or ELSS Mutual Funds for 2015

1. BNP Paribas Long Term Equity Fund 2. Axis Tax Saver Fund 3. IDFC Tax Advantage (ELSS) Fund 4. ICICI Prudential Long Term Equity Fund 5. Religare Tax Plan 6. Franklin India TaxShield 7. DSP BlackRock Tax Saver Fund 8. Birla Sun Life Tax Relief 96 9. Reliance Tax Saver (ELSS) Fund 10. HDFC TaxSaver

Invest Rs 1,50,000 and Save Tax under Section 80C. Get Good Returns by Investing in ELSS Mutual Funds Online

Invest in Tax Saver Mutual Funds Online For further information contact Prajna Capital on 94 8300 8300 by leaving a missed call --------------------------------------------- Leave your comment with mail ID and we will answer them OR You can write to us at PrajnaCapital [at] Gmail [dot] Com OR Leave a missed Call on 94 8300 8300 |

| Posted: 10 Nov 2015 03:57 AM PST Increase or Improve your CIBIL Score / Rating?Apart from your income, your credit worthiness is the single most important tool considered by Loan providers while evaluating your application for any type of loan. Thus, it becomes utmost important to understand how does your Credit Information Report (CIBIL – Credit Information Bureau India Limited) works and how to improve a bad credit history to increase your credit worthiness. It is generally accepted that a credit score more than 730 is good and educes assurance and trust from banks.

A good CIBIL score / rating can be maintained by following simple rules: Rule 1: Don't be late in paying billsFirst and foremost Rule is to pay your bills and all outstanding like home loan EMI, car loan EMI, credit card payment on time. Every time you miss the payment date, the information of your default is updated by your banks to CIBIL and which makes your CIBIL score uglier every time. It's always so alluring to pay the minimum balance of your credit card and pay the remaining balance later on but neither does this practice save you from interest nor does it stop your banks from updating your default payment in CIBIL. Always try to pay your bills one or two days before the due date if you pay through online medium but in case you use cheque to pay your bills than try to drop it a week earlier so even in case of any holiday or sudden shut down of banking operations you will remain safe. Rule 2: Do not utilize all your Credit LimitsNever go using your entire credit limit, try to minimize it and restrict it to 50% of your limit. For example say you have credit limit of Rs.3 lacs, so keep your usage upto 50% i.e. Rs. 1.5 lakhs instead of fully saturate the whole credit limit. This may be viewed negatively by a Loan provider. Even you pay all your dues on time but utilize full credit limit, the CIBIL score might get affected adversely. In case you hold more than one credit card than use the credit cards simultaneously. Using one card to fullest and second to none does not seems to be a bonafide practice. Rule 3: Escape from Being "Credit Hungry"Making many applications for loan either for car, home, marriage etc. in a short span of time or shortly after you have been sanctioned a new credit loan, likely to draw attention of a Loan provider to view your all further applications with caution, treating you as "Credit Hungry". Since your debt burden is likely to increase, your chances of getting additional debts reduce. Rule 4: Consolidate your CreditsThere was a time when people used to keep more and more credit cards just to show off how rich s/he is but that was past, because that time banks did not issue credit cards of much higher limit. But today it is highly suggested that rather having 5 or 6 cards having credit limits of Rs. 20,000 each, get one card having limit of Rs.1 lacs. This way you would be standing on equal credit limit but with less number of worries to remember the due date of payment of each credit card. The same practice can be used with loans having one larger loans is considered much better than having number of small loans. Approach the bank and give details on all these loans and you can transfer the balance outstanding. Rule 5: Duration of Credit HistoryThis rule can be well understood by sneaking in personal life, purity of relationship cannot be judged in a short term, one need a considerable time to know how much the other person can be trusted. Same goes with your credit history, taking short term loan in regular interval and repaying them does not enhance your credit limit. If you are in need than take a 5 or more year loan and then repay it without fail. This will increase your CIBIL rating and also your credit worthiness in the eyes of bankers. Rule 6: Settling DisputesEver had any disputes with banker?? Many of us had or still have. Don't opt settlement path in this case because such settled loan accounts spoil your credit score. Better site with the bank and try to solve it harmoniously. Be open to disagreements and face the weaker links in the dispute. Rule 7: Don't be a guarantor to defaulterThis is not easy in case your friend approach you to be his guarantor and you know that he is at present indebted to you. But keep in mind that if he defaults on payment you are held liable and your score will go down. Don't do it, unless you are really sure you want to do it. Rule 8: PatienceIncreasing or improving your bad CIBIL score is a slow process that takes about 8-12 months to start reflecting in your CIBIL report if you religiously follow the steps I have mentioned in this article. And after about 8 months, check your CIBIL report first before applying for any loans or credit card. You will be able to see the difference yourself. Best Tax Saver Mutual Funds or ELSS Mutual Funds for 2015

1. BNP Paribas Long Term Equity Fund 2. Axis Tax Saver Fund 3. IDFC Tax Advantage (ELSS) Fund 4. ICICI Prudential Long Term Equity Fund 5. Religare Tax Plan 6. Franklin India TaxShield 7. DSP BlackRock Tax Saver Fund 8. Birla Sun Life Tax Relief 96 9. Reliance Tax Saver (ELSS) Fund 10. HDFC TaxSaver

Invest Rs 1,50,000 and Save Tax under Section 80C. Get Good Returns by Investing in ELSS Mutual Funds Online

Invest in Tax Saver Mutual Funds Online For further information contact Prajna Capital on 94 8300 8300 by leaving a missed call --------------------------------------------- Leave your comment with mail ID and we will answer them OR You can write to us at PrajnaCapital [at] Gmail [dot] Com OR Leave a missed Call on 94 8300 8300 |

| Posted: 10 Nov 2015 03:10 AM PST Systematic Investment Plan (SIP) route is one of the best approaches of investing in Mutual Funds for a common man. SIP enables an investor to involve in the stock market but at lesser risk.

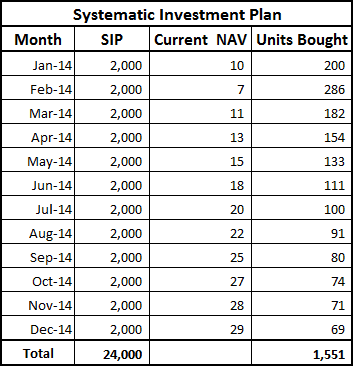

What is Systematic Investment Plan (SIP)?SIP is similar to Recurring Deposits where you have to deposit a predetermined amount (minimum of Rs.500) each month for a stipulated time period in a particular mutual fund scheme. What is the Sole Benefit of Systematic Investment Plan (SIP)?The main advantage of adopting SIP route is to average out the cost of purchase over the time as it enables you to buy mutual funds units at different levels and you can take the advantage of lower prices. Let's understand this with an example.

Average NAV works out to be (110+7+11+13+15+18+20+22+25+27+28+29)/12) =Rs.18.75/- Average Purchase Cost of MF Units (24,000/1551) =Rs.15.48/- Mr.A invests Rs.2,000 for twelve months through SIP. As we can see the average purchase cost of mutual fund units works out to be Rs.15.48 per unit which is lower than average NAV of Rs.18.75 per unit. As you have understood the concept of SIP, it's time to see how to maximize returns through SIP route of investment in mutual funds. How to Maximize your Mutual Fund SIP Returns?1. Stay Put for Long TermPeople tend to invest when market surges and stop when market plunges but this practice defeats the basic purpose of investing through SIP. Staying Invested over the Complete Market Cycle enables you to even out the market volatility and allows you to bank the advantage of lower prices. By exiting during the market slump, you forgo the advantage of buying additional units of mutual fund because per unit value falls when market crashes. These additional units could give you an edge when market bounce back and may prove the decisive point of holding the concerned mutual fund. So you should hold the mutual fund for at least 3 years till the market cycle complete to benefit from the SIP. 2. Hold Sufficient Number of Mutual Funds in PortfolioDiversification can be achieved by having 3 to 5 mutual fund schemes in your portfolio. You should not have more than 5 mutual funds unless you have surplus money and want to dip all your fingers into share market. For example if you wish to start SIP of Rs.7,000 per month then instead of putting Rs.1,000 in 7 schemes, you can invest for Rs.1,500 in four and Rs.1,000 in one scheme to maintain the diversification of your portfolio. Apart from the number of mutual funds, you should also ensure that all your mutual funds are not targeting the same sector means if one of your mutual funds majorly holds shares of banking sector then make sure that other mutual fund schemes in your portfolio are targeting different sectors. 3. Step-Up SIP ApproachNothing is Constant nor should your SIP. With the rise in your income your savings will go up. So your SIP amount should also increase in the same proportion. The increment is not necessarily be invested into new scheme you can allocate the increased amount into existing mutual funds also. The step-up SIP approach is useful to adjust the return according to inflation and to keep pace with changing lifestyle. For example, if you invest Rs.5,000 per month and increase this amount by 10% per annum, your corpus would shoot up by 45% from Rs.11.61 lakhs to Rs.16.87 lakhs in a time period of 10 years. 4. Choose Multiple Investment Date for SIPWe all know that Indian Share Market is too volatile and may give jolts at any point of time. Nobody can ascertain the specific time of upward and downward movement of the market. That's why share market trading is not a child's play. Market volatility indirectly impacts mutual fund performance, thus to mitigate this impact you should fix the SIP at different dates of month. For instance if you have 5 mutual funds in your portfolio, then you could fix different SIP dates for each of the mutual fund like 1st, 8th, 14th, 21stand 28th. So if market goes down on 8th, only one of your mutual fund schemes gets affected. 5. Link SIP to Financial GoalsAs an old saying that "A Goal without Plan is just a Wish", so your every investment plan should be backed by the Goal. The goals could be of short-term like going on vacation, buying a car etc. or long-term such as children education, children marriage, retirement etc. Selection of mutual funds must be based on this and every mutual fund SIP should be linked to one financial goal. You should target Debt Oriented Mutual Funds for your short-term goals because the time horizon is less and safety should be your first concern. Likewise, you should target Equity Oriented Mutual Funds for your long-term goals because the time horizon is not a problem so you could take some risk here. 6. Review Mutual Fund Portfolio every 6 monthsMutual Fund performance is based on various national and international factors. Any Deviation in these factors may affect the performance of scheme. For example last year Rupee value depreciated to Rs.68 per Dollar which made IT services and Pharma Sector most favorable. Likewise, the New Central Government is focusing on ""Housing for all by 2022", this makes infrastructure sector a preferred choice for every mutual fund manager. Ranking and return of the scheme is thoroughly based on the alteration made by mutual fund manager. Similar to the mutual fund manager you should also review your portfolio twice in a year and switch from the mutual fund scheme whose return and ranking is decreasing constantly. This is the indication of getting out of that mutual fund scheme and invests in new scheme from the same category. 7. Use Systematic Transfer/Withdrawal PlanSystematic Transfer Plan (STP) means transferring fixed amount from one type of fund to another. STP can be used when you have large chunk of money in your bank. Instead of parking money in Bank, you can transfer money into liquid funds and then get a fixed amount transferred into chosen equity funds via STP. This transfer of money from bank to liquid funds and then liquid funds to equity funds will maximize your returns. You can also use Systematic Withdrawal Plan (SWP) when you are getting near to your financial goal. That time it is not advisable to stay put in the riskier equity funds. You can start SWP to withdraw a fixed amount by redeeming your mutual fund units. If you don't want to redeem units you can also go for an STP wherein you can get a fixed amount transferred from equity mutual funds to debt mutual funds which is less riskier and more stable option of protecting your gains and ensure the realization of your financial goal. Words of Wisdom Share Market risk in inherent and no one can escape from it. As we all know the concept of "No Risk No Reward" but by following the above tips you can mitigate the risk and maximize returns. Best Tax Saver Mutual Funds or ELSS Mutual Funds for 2015

1. BNP Paribas Long Term Equity Fund 2. Axis Tax Saver Fund 3. IDFC Tax Advantage (ELSS) Fund 4. ICICI Prudential Long Term Equity Fund 5. Religare Tax Plan 6. Franklin India TaxShield 7. DSP BlackRock Tax Saver Fund 8. Birla Sun Life Tax Relief 96 9. Reliance Tax Saver (ELSS) Fund 10. HDFC TaxSaver

Invest Rs 1,50,000 and Save Tax under Section 80C. Get Good Returns by Investing in ELSS Mutual Funds Online

Invest in Tax Saver Mutual Funds Online For further information contact Prajna Capital on 94 8300 8300 by leaving a missed call --------------------------------------------- Leave your comment with mail ID and we will answer them OR You can write to us at PrajnaCapital [at] Gmail [dot] Com OR Leave a missed Call on 94 8300 8300 |

| You are subscribed to email updates from Prajna Capital - An Investment Guide. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

ReplyDeleteatal pension yojana chart